Cost estimation is a fundamental component of housing development, involving the systematic calculation of quantities and costs of materials, labor, equipment, and overheads required for construction. Accurate estimation ensures financial feasibility, efficient resource allocation, and timely project execution. In the context of housing—ranging from affordable housing to high-income residential units—cost estimation plays a vital role in planning, budgeting, and policy implementation.

The determination of rates involves analyzing unit costs of construction components, including materials, labor, transportation, and contractor profit margins. These rates vary depending on housing type, location, construction technology, and market conditions.

2. Objectives of Cost Estimation

- To determine the total construction cost of housing projects

- To prepare budgets and financial plans

- To evaluate project feasibility

- To assist in tendering and contract management

- To control costs during construction

- To compare different housing alternatives

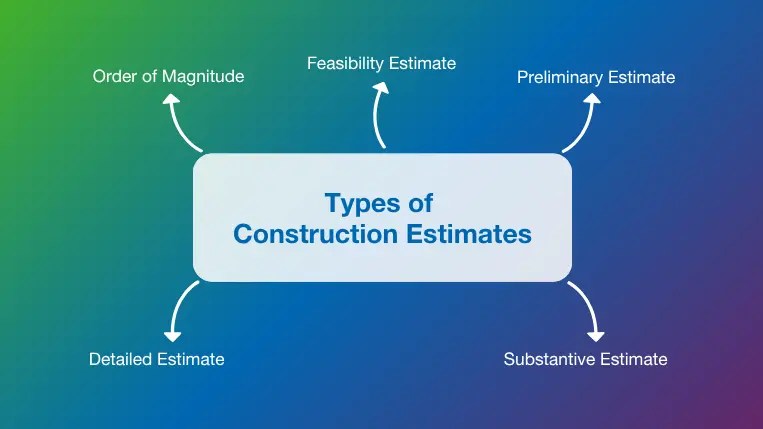

3. Types of Cost Estimates

3.1 Preliminary Estimate (Approximate Estimate)

- Prepared at the planning stage

- Based on plinth area or carpet area

- Used for feasibility analysis

3.2 Detailed Estimate

- Prepared after final design

- Includes item-wise quantities and costs

- Basis for tendering

3.3 Revised Estimate

- Prepared when cost exceeds original estimate

- Reflects design or price changes

3.4 Supplementary Estimate

- Prepared for additional works not included earlier

4. Methods of Cost Estimation

4.1 Plinth Area Method

- Cost = Plinth Area × Rate per sq.m

Example

- Plinth area = 100 sq.m

- Rate = ₹18,000/sq.m

- Total cost = ₹18,00,000

Advantages

- Simple and quick

- Suitable for preliminary estimates

Limitations

- Less accurate

- Does not consider design complexity

4.2 Carpet Area Method

- Based on usable floor area

- More accurate for residential units

4.3 Cubic Content Method

- Based on volume (length × breadth × height)

- Useful for multi-storey buildings

4.4 Detailed Quantity Take-off Method

- Most accurate method

- Based on actual quantities of work

5. Components of Housing Cost

5.1 Direct Costs

- Materials (cement, steel, bricks, sand)

- Labor (skilled and unskilled)

- Equipment

5.2 Indirect Costs

- Supervision

- Site office expenses

- Temporary works

5.3 Overheads

- Administrative expenses

- Insurance

- Taxes

5.4 Contractor’s Profit

- Typically 10–15%

6. Determination of Rates (Rate Analysis)

Rate analysis is the process of determining the cost per unit of work (e.g., per cubic meter of concrete, per square meter of plaster).

6.1 Components of Rate Analysis

(a) Material Cost

- Quantity of materials required

- Market rates

(b) Labor Cost

- Skilled, semi-skilled, unskilled labor wages

(c) Equipment Cost

- Machinery and tools

(d) Transportation Cost

- Material delivery to site

(e) Overheads and Profit

- 10–15% added

6.2 Example: Rate Analysis for Brick Masonry (1 m³)

| Component | Quantity | Rate (₹) | Cost (₹) |

|---|---|---|---|

| Bricks | 500 nos | 8 | 4000 |

| Cement | 1.5 bags | 400 | 600 |

| Sand | 0.3 m³ | 1200 | 360 |

| Labor | Lump sum | — | 1500 |

| Total | — | — | 6460 |

| Add 10% profit | — | — | 646 |

| Final Rate | — | — | ₹7100/m³ |

7. Types of Housing and Cost Characteristics

7.1 Economically Weaker Section (EWS) Housing

Features

- Small unit size (25–40 sq.m)

- Basic amenities

- Low-cost materials

Cost Range

- ₹8,000 – ₹15,000 per sq.m

Cost Reduction Strategies

- Use of locally available materials

- Precast components

- Standardized designs

7.2 Low-Income Group (LIG) Housing

Features

- Unit size: 40–60 sq.m

- Basic facilities with improved finishes

Cost Range

- ₹12,000 – ₹20,000 per sq.m

7.3 Middle-Income Group (MIG) Housing

Features

- Unit size: 60–120 sq.m

- Better materials and finishes

Cost Range

- ₹18,000 – ₹30,000 per sq.m

7.4 High-Income Group (HIG) Housing

Features

- Large units (>120 sq.m)

- Premium materials and amenities

Cost Range

- ₹30,000 – ₹60,000+ per sq.m

8. Factors Affecting Housing Cost

8.1 Location

- Urban vs rural

- Land cost variations

8.2 Material Prices

- Cement, steel fluctuations

8.3 Labor Cost

- Skilled labor availability

8.4 Design Complexity

- Architectural features

- Structural design

8.5 Construction Technology

- Conventional vs prefabrication

8.6 Government Policies

- Subsidies

- Taxes (GST)

9. Standard Schedule of Rates (SOR)

- Prepared by CPWD/PWD

- Provides standard rates for materials and labor

- Used for estimation and tendering

10. Cost Optimization Techniques

- Value engineering

- Use of alternative materials

- Efficient design planning

- Bulk procurement

11. Example: Cost Estimation of a Small House

Given

- Plinth area: 80 sq.m

- Rate: ₹20,000/sq.m

Calculation

- Total cost = 80 × 20,000 = ₹16,00,000

Cost Distribution

| Component | Percentage | Cost (₹) |

|---|---|---|

| Foundation | 10% | 1,60,000 |

| Superstructure | 40% | 6,40,000 |

| Finishing | 25% | 4,00,000 |

| Services | 15% | 2,40,000 |

| Miscellaneous | 10% | 1,60,000 |

12. BOQ (Bill of Quantities)

A BOQ lists all items of work with quantities and rates:

- Earthwork

- Concrete

- Masonry

- Plastering

- Flooring

- Painting

13. Role in Housing Policy and Planning

- Supports affordable housing schemes (PMAY)

- Helps in subsidy calculation

- Assists urban planners in project evaluation

14. Challenges in Cost Estimation

- Price fluctuations

- Inaccurate quantity estimation

- Delays and cost overruns

- Lack of skilled labor

15. Conclusion

Cost estimation and rate determination are essential for successful housing development. Different housing categories—EWS, LIG, MIG, and HIG—have distinct cost structures influenced by materials, design, and amenities. Accurate estimation ensures financial viability, efficient construction, and effective policy implementation. Adoption of modern techniques and sustainable practices can further optimize costs and improve housing affordability.

You must be logged in to post a comment.