Every single item we order does not have equal value. Some parts cost more. Some are used more frequently. Some are both. ABC inventory analysis helps categorize those items so we can understand which ones should receive our full attention.

As the name suggests, this inventory categorization technique groups your inventory in three buckets: A, B, & C.

- A’ items are the most important to an organization. This material should receive your full focus due to its high usage rate or a high price (or both).

- ‘B’ items have a lower dollar volume and are thus less important than ‘As’.

- Finally, ‘C’ items are the low rung on the ladder. Out of the three groups, you’ll have the highest number of ‘C’ items, but they will account for the lowest portion for your inventory value.

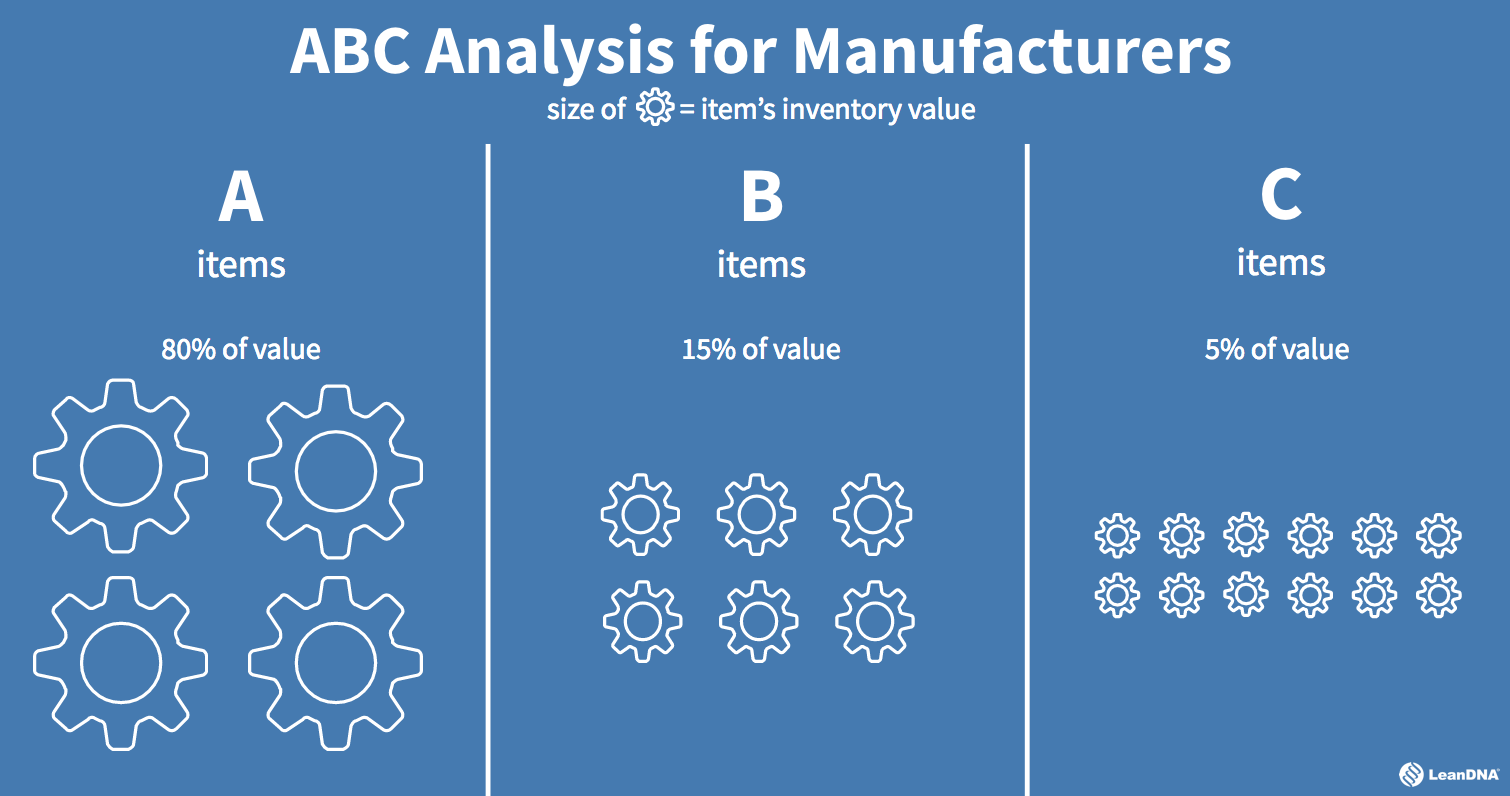

The pareto principle states that 80% of your inventory costs comes from just 20% of your inventory. This is known as the 80/20 rule and it helps shape the results of your ABC Analysis. LeanDNA recommends the following breakdown as the optimal way to determine the three categories:

- ‘A’ items – 80% of the annual inventory value of your items (likely made up of just 20% of your items)

- ‘B’ items – 15% of the annual inventory value of your items (likely made up of 30% of your items)

- ‘C’ items – 5% of the annual inventory value of your items (likely made up of 50% of your items)

ABC analysis has a lot of similarities to RRS analysis – “Runner, Repeater, Stranger analysis,” that is. Runners are your ‘A’ items, Repeaters are your ‘B’ items, and Strangers are your ‘C’ items.

In order to determine which parts fall into which categories, use the following steps:

- Determine inventory value by multiplying the price of an item by the consumption volume of that item in a year period. Simply put, item cost * annual consumption = inventory value.

- Repeat step 1 for all items to calculate total inventory value.

- Sort your parts from highest inventory value to lowest.

- Calculate each item’s percentage of total inventory value. That item’s inventory value / sum of all inventory values = item % of total inventory value.

- Group the parts that account for the highest 80% of your total inventory and allocate them as ‘A’ items. Group the parts that account for the next 15% and allocate them as ‘B’ items. Group all remaining items as ‘C’.

You must be logged in to post a comment.